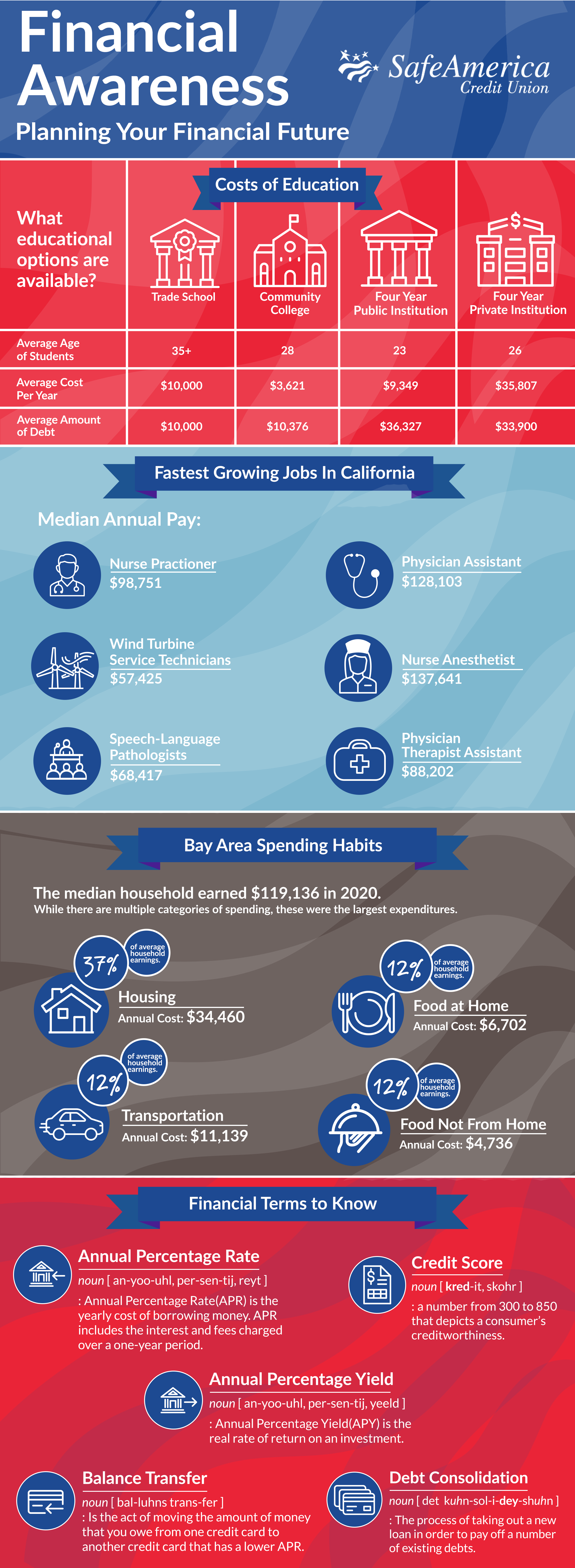

Debt can be a challenge to manage, even in the best of times. Now, with the economy in the news nearly every day, how do you effectively manage your debt as the cost of borrowing for things like homes, cars,

and credit cards rises? People are successful when they set a realistic budget for spending. Focusing on non-traditional gifts, the joy of experiences and the resulting memories, can be just as rewarding without damaging your finances, especially as prices on essentials are rising.

Here are five general questions to ask in order to minimize the hit to your wallet in the face of rising interest rates.

What's Your Current Credit Score And History?

Knowing this information helps you understand how rising interest rates will apply to you. Some research shows that only 33 percent of Americans checked their credit score in the past year. Regularly monitoring your credit can alert you to errors, protect you from fraud, and provide you valuable information to strengthen your credit score–which can potentially minimize the rising cost of borrowing.

What Is Your Debt Portfolio?

Another helpful course of action is to make a list of your current debt such as credit cards, car loans, student loans and other debt. Although it’s a simple step, this can make a big difference in visualizing the big picture of your financial situation. Part of seeing the impact of rising interest rates is understanding exactly where you stand.

What Are Your Current Interest Rates?

An effective next step is to regularly review your balances, terms, and interest rates on a monthly basis. By staying on top of this vital information, you can make adjustments and informed decisions about reducing any existing balances more aggressively. As a debt paydown strategy, it often makes sense to start with the highest interest credit cards or loans.

What Is A Realistic Payment Plan?

As you are able, consider paying credit card balances in full by the due date each month. You can avoid interest charges on what you purchase, which means rising interest rates may not have much of an effect on your household finances.

What Is Your Overall Financial Plan?

To stay financially healthy and minimize the impact of rising interest rates, it is key to earn more than you spend, so that you have enough money to build savings for the future. Keeping an eye on your spending is an important step in the effort to create a budget without the cost of high-interest debt. Once you develop a household budget and track income and spending, it becomes clear where the money is going and where you need to adjust your spending to achieve your financial goals. By setting financial goals, preparing a financial plan, sticking to a budget, and setting up an emergency fund for the unexpected, you ensure that your financial well-being does not suffer as interest rates rise.

This information brought to you by GreenPath Financial Wellness.