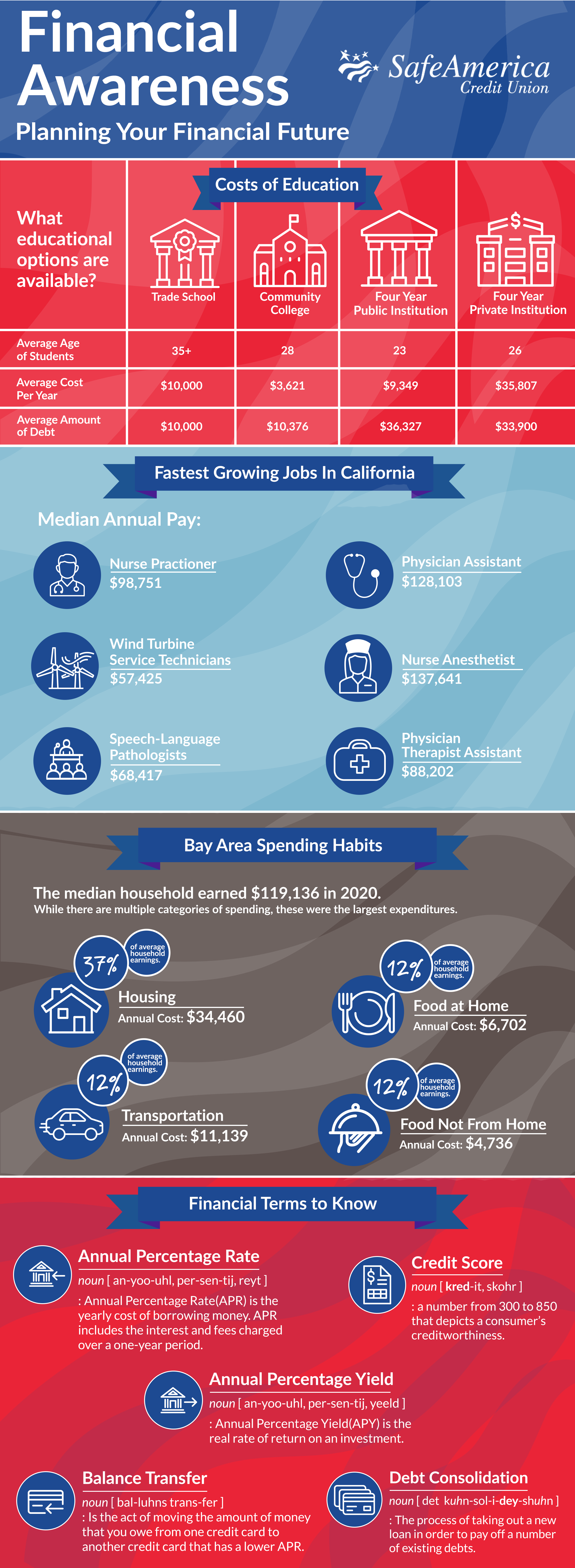

Being financially fit can be thought of as performing like an elite athlete on the playing field of your finances. It’s all about money-savvy acrobatics to keep your cash in tip-top shape.

Financial fitness lets you flex those savings muscles! The stronger your savings get, the more you can lift your dreams into reality. Whether it’s a dream vacation or a shiny new gadget, your savings make it happen.

")

Being financially fit also means you’re in the race to win at personal finance. You’ve got the determination, discipline, and enthusiasm to take home the gold medal in money management.

Your financial fitness lets you effectively manage your financial resources, make informed financial decisions, and maintain a stable and healthy financial state. It involves practices such as budgeting, saving, investing, and managing debt to achieve financial goals and withstand unexpected financial challenges.

Financial Fitness Checklist

Credit card debt, high interest rates, and rising prices are just a few factors that can challenge how you think about your financial fitness.

While the short video lifted up steps to get you thinking proactively about your financial future, there are other considerations.

To guide those looking to achieve financial goals, this five-part checklist is a way to break the steps down for success.

How did you do on the checklist shared in the video above? Are you working through the items sometimes, all of the time, or never?

1. Track Monthly Spending

Staying financially fit begins with ensuring you earn more than you spend, so that you have enough money to build savings for the future. Keeping an eye on your spending is an important step in the effort to create a budget that builds. Once you develop a household budget and track income and spending, it becomes clear where the money is going and where you need to adjust your spending to achieve your financial goals.

If you take the time to manage financial tasks, you will start to develop financial fitness. This includes making sure that your bills are paid, that you have saved money for emergencies and that your financial strategy for the future is on track.

With this helpful online worksheet, getting a current snapshot of monthly money will help as you create a plan to increase financial fitness.

2. Set Goals

If you are saving for an emergency home purchase or paying off high-interest debt, a simple plan will help you meet your goals. As an example, by managing debt, you ensure that your financial well-being does not suffer.

It is not uncommon for people with credit card debt to only pay the interest on the amount borrowed, instead of planning to eliminate the debt altogether. When considering your overall financial picture, consider a debt management plan.

3. Know Your Credit History

Another tip from the financial fitness checklist is to pull all three of your credit reports each year. It is easier than you might think.

Checking your credit history can reveal any inaccuracies or issues you might want to resolve. If you find inaccuracies or errors in your credit report, you can dispute them with the credit reporting agencies. Addressing these issues promptly can help improve your credit profile and prevent potential obstacles in the future. Each person’s situation is unique when it comes to credit history and score, a key part of financial well-being.

4. Build a Savings Habit

Setting and sticking to a realistic savings plan is another key component of financial fitness. You can automate savings directly from your employer or put into place other tricks to make it a seamless savings process. No matter the amount, setting aside a budget-friendly amount each month for savings builds fitness and financial health.

5. Connect with Trusted Resources

When it comes to financial fitness, you are not alone. The trusted national nonprofit GreenPath offers the expertise of caring, NFCC-certified financial counselors who are trained to understand your unique financial situation and provide personalized solutions. GreenPath’s caring counselors can help you create a comprehensive plan to manage your debts effectively. In addition, nonprofit credit counseling agencies such as GreenPath offer educational resources, online webinars, and tools to help you understand the fundamentals of personal finance. This empowers you to make better financial decisions in the future.

Why Work Towards Financial Fitness?

Imagine your finances as a well-tuned engine powering your life. When that engine runs smoothly, you have the freedom to do the things you love and handle any unexpected bumps in the road with confidence. Here’s why being financially fit matters:

Less Stress, More Peace: When you have control over your money and know that your bills are covered, it’s like a weight lifted off your shoulders. You can sleep better at night and enjoy a more peaceful, stress-free life.

Freedom to Pursue Dreams: Being financially fit gives you the ability to chase your dreams and passions. Whether it’s traveling the world, starting your own business, or buying a home, having the financial means makes those dreams attainable.

Security During Emergencies: Life throws curveballs, and having a financial cushion means you’re ready for them. Whether it’s a medical emergency, unexpected car repair, or a sudden job loss, being financially fit means you can weather these storms without losing your footing.

Retirement Comfort: Financial fitness ensures that you can retire comfortably when the time comes. You won’t have to rely solely on social security or work during your golden years, giving you the freedom to relax and enjoy life.

Building Wealth: It’s not just about getting by; it’s about thriving. Being financially fit allows you to save and invest, which can grow your wealth over time, giving you more options and opportunities.

Reduced Debt Burden: Financial fitness often involves managing and reducing debt. Lower debt means less money going toward interest payments and more money for you to use as you see fit.

Peace of Mind for Loved Ones: If you have a family or dependents, being financially fit means you’re providing security and a better future for them as well.

Final Thoughts About Your Financial Checklist

As with a healthy diet, we maintain our physical fitness in the same way, and if we follow this checklist shared in the materials above, we can return to financial fitness with a little help and a clear strategy.

It is always a good time to understand where you are financially and get help to keep things on track. Caring, certified counselors from the trusted national nonprofit GreenPath Financial Wellness can help you get started on your financial journey and then, keep going.

In the end, financial fitness isn’t about having tons of money; it’s about managing the money you have wisely. It’s a journey, not a destination. So, take small steps, make good financial habits, and watch how it transforms your life for the better.

This information is brought to you by our partners at GreenPath Financial Wellness